A PR friend sent this WWD article to me for my interest, and while I don't know her position, I do know that this will be viewed as something that is not viable, or as a way for a designer to make money. In my opinion, this is a great way to stop the bleeding from sending samples everywhere without ever getting them back. Not to mention the shipping costs that are not recouped. Here is the article from WWD:

GOOD LUCK WITH THAT: Lots of designers have trimmed their budgets for press samples lately, but James Perse is going to an extreme, making editors purchase products in order to shoot it. Under the brand’s new policy, euphemistically named the “Studio Sales Discount,” editors must prepay by credit card for product, minus a 10 percent discount. They have 10 days, not a day more, to return the product for a refund, minus a 20 percent restocking fee. James Perse will not accept returns of T-shirts, (which are its bread and butter,) undergarments, footwear or bathing suits. Apparently, the company has decided an editorial credit isn’t worth more than 30 percent of the cost of a T-shirt. Returns will only be processed by the brand’s Melrose Avenue store in Los Angeles — not a showroom or press office. Still interested, editors? The first step is to fill out a credit application. Later on, if you need to transfer the account to a colleague or a successor, you will be required to notify James Perse by certified mail.

This really shows the skeptical view of PR, the effort involved, and the unguaranteed sales from it. Yet, PR by certain outlets opens doors to other outlets and even stores. Not to mention the people swayed by what they see in the glossies. It also might give a nod to the power of the internet and word of mouth sales, banking on the presence that designers can build for themselves with a lot of effort.

Mista Readers: What do you think?

Showing posts with label Money Stuff. Show all posts

Showing posts with label Money Stuff. Show all posts

CareCredit for Laser Hair Treatment :: Be Alert!!

Mistas - You know that I signed up for the promotional CareCredit card through GEOnline when I got my laser hair removal package. It was the 0% APR for a year deal. If I paid the whole thing off within a year, I would not pay the APR fees. What I did NOT know, was that if I did NOT pay it in a year, the DEFERRED APR fees will be charged of me.

Yuck!

When it comes to savviness with credit cards, I am OK. I'm not super savvy, but I do make sure to make all payments on time, and I transfer my one large balance to new 0% APRs after the first year of the promotional date. However, I've never had the situation where I pay the deferred finance charge. When I got my cool glasses through a similar card through City Bank, who is the Devil, when I was paying a bill, I noticed the tiny fine print about a deferred finance charge. But the message was a little cryptic. Not trusting it, I transfered it right away to my big 0% APR card to get rid of any unexpected finance charge. This must have been what they were talking about.

Here's the message I've been getting on my CareCredit statements. Keep in mind, this is a "health" credit card, so they encourage you to use it for the vet, dentist maybe, healthy stuff. Luckily I kept it in my file of Unused Credit Cards Waiting to be Paid Off and never in my wallet.

"No Finance Charges will be incurred on the amount of a Deferred Interest promotional purchase if you pay the promotional purchase amount in full by the indicated Due Date and (as applicable) you pay at least any Minimum Payment Due on your Account each month when due. If a promotional purchase amount is not paid in full by the indicated Due Date, Finance Charges will (or if any Minimum Payment Due is not paid when due, may) be assessed on this amount from the transaction date (or, at creditors option, from the posting date)."

The total deferred finance charge is shown below this statement, but I always thought it was a way to show me what I saved. Duh. Wrong.

Don't know about you, but that's not exactly easy and clear for me to understand. CareCredit has since changed the design of their statement. It now says this, which has alerted me more clearly. It now says this:

"You will incur no Finance Charges on a Deferred Interest promotional purchase, provided the promotional purchase amount is paid in full by the indicated Due Date and you pay any applicable Minimum Payment Due on your Account by the Payment Due Date. If you do not pay the amount in full by the indicated Due Date, Finance Charges accrued from the date of purchase will (or if any Minimum Payment is not paid when due, may) be added to your account."

I'm still a little foggy on this, but even as I type it, I think I just understood a new meaning. Shoot. It says that not only will I have to pay the deferred finance charge if I don't pay it off by my year date, which so far for me is $309.47, if I missed any minimums, which I did once and maybe twice because I swear that their statements are sent on a longer than 30-day rotation period, I may also have to pay it. Ahh!

So Mistas - be super aware of these promotional deals. I of course paid way more than the minimum payment, and last month basically double paid my amount, which is 4x the minimum, so I'm finally under $1000 due. Yay. But this baby better get paid by me in two months, or you will be hearing a very unhappy FashionMista.

Home | Link to this

Yuck!

When it comes to savviness with credit cards, I am OK. I'm not super savvy, but I do make sure to make all payments on time, and I transfer my one large balance to new 0% APRs after the first year of the promotional date. However, I've never had the situation where I pay the deferred finance charge. When I got my cool glasses through a similar card through City Bank, who is the Devil, when I was paying a bill, I noticed the tiny fine print about a deferred finance charge. But the message was a little cryptic. Not trusting it, I transfered it right away to my big 0% APR card to get rid of any unexpected finance charge. This must have been what they were talking about.

Here's the message I've been getting on my CareCredit statements. Keep in mind, this is a "health" credit card, so they encourage you to use it for the vet, dentist maybe, healthy stuff. Luckily I kept it in my file of Unused Credit Cards Waiting to be Paid Off and never in my wallet.

"No Finance Charges will be incurred on the amount of a Deferred Interest promotional purchase if you pay the promotional purchase amount in full by the indicated Due Date and (as applicable) you pay at least any Minimum Payment Due on your Account each month when due. If a promotional purchase amount is not paid in full by the indicated Due Date, Finance Charges will (or if any Minimum Payment Due is not paid when due, may) be assessed on this amount from the transaction date (or, at creditors option, from the posting date)."

The total deferred finance charge is shown below this statement, but I always thought it was a way to show me what I saved. Duh. Wrong.

Don't know about you, but that's not exactly easy and clear for me to understand. CareCredit has since changed the design of their statement. It now says this, which has alerted me more clearly. It now says this:

"You will incur no Finance Charges on a Deferred Interest promotional purchase, provided the promotional purchase amount is paid in full by the indicated Due Date and you pay any applicable Minimum Payment Due on your Account by the Payment Due Date. If you do not pay the amount in full by the indicated Due Date, Finance Charges accrued from the date of purchase will (or if any Minimum Payment is not paid when due, may) be added to your account."

I'm still a little foggy on this, but even as I type it, I think I just understood a new meaning. Shoot. It says that not only will I have to pay the deferred finance charge if I don't pay it off by my year date, which so far for me is $309.47, if I missed any minimums, which I did once and maybe twice because I swear that their statements are sent on a longer than 30-day rotation period, I may also have to pay it. Ahh!

So Mistas - be super aware of these promotional deals. I of course paid way more than the minimum payment, and last month basically double paid my amount, which is 4x the minimum, so I'm finally under $1000 due. Yay. But this baby better get paid by me in two months, or you will be hearing a very unhappy FashionMista.

Home | Link to this

First SuperNova on the Debt-O-Meter!

This just in! A small supernova on the Debt-O-Meter! The balance was small, but its story was not. National City, who I am not a fan of and if you work there this is nothing personal, slammed my checking account with charges after their misleading voice-operator guy led me to believe I always had money in my account, which had some small direct deposits hooked up to it. Although I got statements in the mail, I did not read them (bad, FashionMista). They told me that I was living in my line-of-credit, and not only had I been living in it, I had exceeded it. They were now charging me for every purchase. I only made small purchases with this card, knowing that it was an emergency account. So every Starbucks half-caff-one-pump-vanilla latte cost me $3.68 + a $36 fine for debiting a purchase to funds that were not available. Unlike credit card companies, National City allowed me to keep charging, gladly taking 11 fines at $36 each instead of putting the "Declined" mark on my account. I would have much rather faced humiliation with a cashier than pay over $400 in fines. Upon this supernova, I have extatically closed this account.

This just in! A small supernova on the Debt-O-Meter! The balance was small, but its story was not. National City, who I am not a fan of and if you work there this is nothing personal, slammed my checking account with charges after their misleading voice-operator guy led me to believe I always had money in my account, which had some small direct deposits hooked up to it. Although I got statements in the mail, I did not read them (bad, FashionMista). They told me that I was living in my line-of-credit, and not only had I been living in it, I had exceeded it. They were now charging me for every purchase. I only made small purchases with this card, knowing that it was an emergency account. So every Starbucks half-caff-one-pump-vanilla latte cost me $3.68 + a $36 fine for debiting a purchase to funds that were not available. Unlike credit card companies, National City allowed me to keep charging, gladly taking 11 fines at $36 each instead of putting the "Declined" mark on my account. I would have much rather faced humiliation with a cashier than pay over $400 in fines. Upon this supernova, I have extatically closed this account.supernova up close

debri from supernova falling into kitchen sink

Must go now. Dinah is crawling into the art supply drawer...

>Home | Permalink

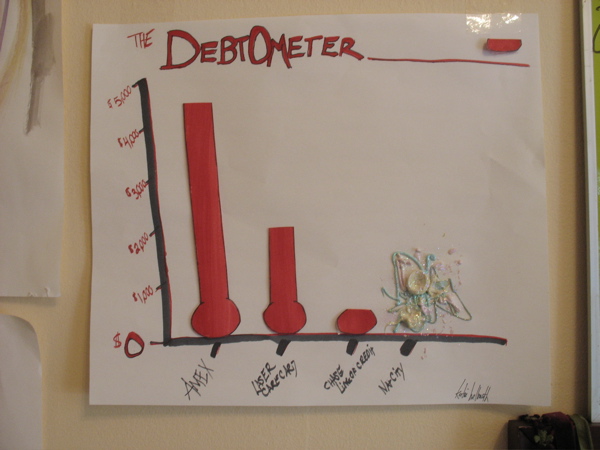

Star Charts and DebtOMeters

David always talked about how much he exercised, when I was the one running every morning with Gerdy. I questioned his statements, so I decided to chart "our" progress with a Star Chart. It gives us gold stars for 20 minutes of cardio, green stars for 10 minutes of calesthetics, red stars for 20 minutes of calesthetics (never happens), and silver stars for long periods of cardio, like biking, that don't make us huff and puff like running a mile would. Wouldn't cha know, I think he's running a bit more, instead of saying "Oh, I'll do it tomorrow night." He comes in now after the run and says: "Did you put my star up?" Hehe.

Jogging every morning is not so hard for me to do, because I have to take Gerdy out anyway, so might as well. But getting my debt down, now that's a problem! It's just not going anywhere. I've stopped charging major stuff, like fabric on a whim (wimper) and queen size mattresses (had to!), but an occasional year's supply of contacts will trump the monthly payment I just paid. This isn't a credit problem. I seem to have good credit because I pay everything. And my card is actually at 0% APR because I transfer when I get "0% APR on balance transfers for a year!" and just pay it, but don't use it. So I haven't paid credit card interest for maybe more than 2 years now. But lately, I've got an Amex card, and am happy with it, so when the 0% APR rate expires, I kind of want to keep the card (usually I brutally transfer and drag the now empty card along...). Also, if I go seeking a loan for katie-james.com, I'm not about to budget in debt into my monthly expenses. That's just depressing!

So I made the DebtOMeter. Every payment I make I will snip away from the red mercury tube. And then when it's gone, it will supernova into a giant gold star!! So excited for that day.

Tip: Mom says that you want to keep a low credit limit. The credit card companies like to "reward" you by increasing your credit limit. So keep that in mind as you balance everything out.

Home | Permalink

Subscribe to:

Posts (Atom)